Learn about Value Added Tax (VAT) and when your business needs to start paying it, as well as why they might pay it.

Value Added Tax is a tax that the government levies on the sale of goods and services. All businesses which have reached an annual turnover that is more than the current VAT threshold of £85,000 are required to register for VAT and to complete a quarterly return.

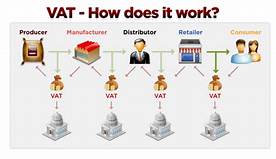

VAT Explained

When you register for VAT you need to do three things: firstly, you must charge VAT (currently 20% for most goods and services) on the things you sell to business and to consumers. Secondly, you must pay VAT on the goods and services that you purchase. Thirdly, you must file a VAT return to HMRC every quarter.

The idea is that the VAT That you pay and the VAT that you charge should be roughly balanced, and you will either pay HMRC any extra VAT you owe, or get a refund for any VAT you have paid in excess.

Practical details for VAT and VAT registration.

- If your turnover for the last twelve months exceeded the VAT Registration threshold then you must register for VAT. The Threshold is currently £85,000 and it is reviewed regularly. You should register if you expect to exceed the threshold soon, too.

- When you add VAT to an invoice you should list it as a separate amount. Show the cost of the good or service before VAT, and then show the cost of the VAT and the rate that you charged it at, as well as the total cost. Look at invoice financing options too.

- VAT can be charged at three different rates – standard rate, reduced rate, and zero rate. Some goods an services are classed as exempt from VAT. Such as antiques or education.

- There are some specific VAT rules which can be applied to certain trades or industries, such as the motor trade.

- You can register to pay VAT via the official www.gateway.gov.uk website.

- The VAT threshold is reviewed as a part of the annual Budget, which is usually announced in March or APril, so you should check each year to make sure that you are charging the right amount and to confirm whether you need to be registered if you are not already.

- You are required to charge VAT on the full sale price of the good or service, even if you are accepting goods in part exchange, or barter.

Key things to Remember

If you sell to another VAT registered business, then you need to add VAT to your invoice, and they will be able to reclaim that VAT. Adding VAT for them is simple because they don’t have to worry about it in the long term. If you have been selling to individual customers for a long time and they are used to your prices, then they may not be happy if the cost of your products goes up by 20%. You may want to take some hit to your margins to cover some or all of the VAT so that you do not lose sales. Since you can reclaim some VAT yourself, this may not work out too badly.

There are three schemes available that can make VAT easier for small businesses.

1 – Flat Rate

If you have a turnover that is less than £150,000 then you can use the Flat Rate VAT scheme. This means that you don’t have to record every transaction. You can simply work out your VAT payments as a percentage of the turnover of your business coming from VAT-eligible items. This saves time, and makes your return quicker and easier. You cannot reclaim VAT on the purchases you make using this scheme, however you do not pay 20% VAT. Rather, depending on the industry you are in your VAT will be applied at a rate of between 9% and 14%.

- Cash accounting

With standard VAT accounting, you pay VAT regardless of whether your customer has already paid the invoice. With cash accounting, you do not pay the VAT until your client pays you. However, you can only perform a VAT reclaim once you have actually paid your own suppliers.

Cash accounting is available to people who have a turnover of less than £1.35 million per year for their businesses. Bigger businesses must follow standard practices.

- Annual accounting

Annual accounting means that you complete a VAT Return and pay the VAT, or get refunds, quarterly. You can use this if you want to keep your paperwork to a minimum. It makes cash flow and accounting much easier. If you are going to use this scheme then you will be asked to make either nine monthly or three quarterly interim payments each year, and then you make one return when the year ends, which will either include a balancing payment or mean that you get a balancing refund. You can use annual accounting if you do not expect your annual turnover to exceed £1.35 million for the year ahead. Bigger businesses will have to follow the original returns procedure.